Dynamic Cash Flow Waterfall Optimization with Structured Finance Constraints

Main KPI: Debt Service Coverage Ratio (DSCR)

Primary Keywords: cash flow waterfall, structured finance, DSCR optimization, preferred equity, mezzanine debt, tranche modeling, covenant constraints, IRR maximization

1. Introduction: Why Cash Flow Waterfalls Are Structurally Complex

Real estate cash flow is not distributed linearly. Institutional assets are typically financed with layered capital structures that include:

Senior mortgage debt

Mezzanine financing

Preferred equity

Common equity

Promote structures

Each layer introduces priority rules that define how cash flows are allocated.

This allocation mechanism is known as the cash flow waterfall, and it is central to:

Equity return forecasting

Debt covenant compliance

Refinancing feasibility

Sponsor promote economics

Risk-adjusted asset optimization

Unlike simple discounted cash flow models, waterfall systems require:

Conditional payment logic

Multi-tranche priority sequencing

Dynamic constraint enforcement

Optimization under uncertainty

Thus, waterfall modeling is fundamentally a structured finance problem.

2. Cash Flow Waterfall Definition

2.1 Asset-Level Cash Flow

Unlevered net cash flow:

CFt=NOIt−CapextCF_t = NOI_t - Capex_tCFt=NOIt−Capext

Levered distributable cash flow:

DCFt=CFt−DebtServicetDCF_t = CF_t - DebtService_tDCFt=CFt−DebtServicet

This distributable amount is then allocated through the waterfall.

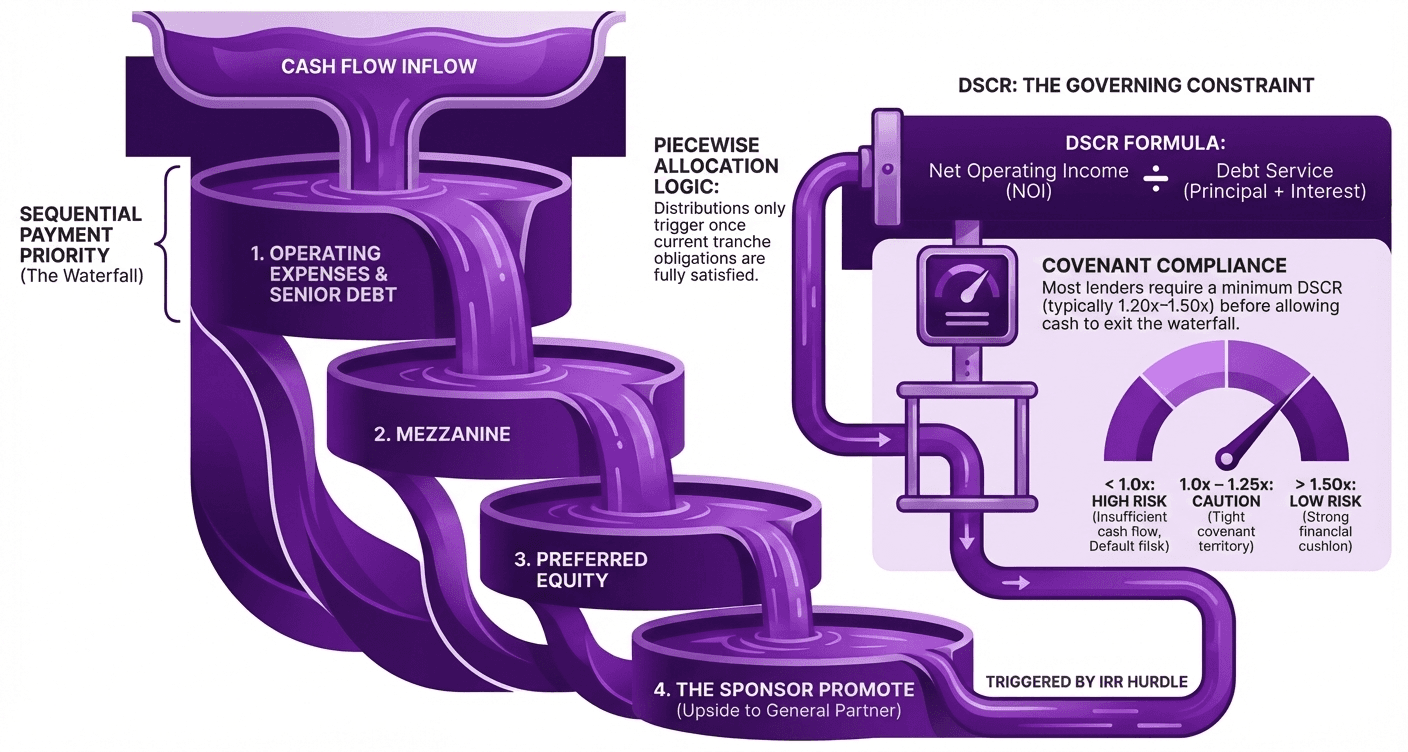

2.2 Waterfall Priority Structure

Typical hierarchy:

Operating expenses

Senior debt service

Reserve accounts

Preferred return to equity

Return of equity capital

Promote split (e.g., 70/30)

Excess cash sweep

This introduces nonlinearity into return outcomes.

3. Main KPI: Debt Service Coverage Ratio (DSCR)

3.1 KPI Definition

DSCRt=NOItDebtServicetDSCR_t = \frac{NOI_t}{DebtService_t}DSCRt=DebtServicetNOIt

Where:

NOItNOI_tNOIt = net operating income

DebtServicetDebtService_tDebtServicet = interest + principal due

3.2 Interpretation

DSCR | Meaning |

|---|---|

<1.0x | Insufficient cash flow (default risk) |

1.0–1.25x | Tight covenant territory |

1.25–1.50x | Healthy coverage |

>1.50x | Strong cushion |

DSCR is the dominant constraint in structured real estate finance.

3.3 DSCR as a Binding Optimization Constraint

Most debt agreements impose:

DSCRt≥DSCRminDSCR_t \geq DSCR_{min}DSCRt≥DSCRmin

Typically:

Multifamily: 1.20x

Office: 1.30–1.40x

Hospitality: 1.50x+

Waterfall optimization must ensure covenant compliance.

4. Structured Capital Stack Architecture

4.1 Senior Debt

Senior mortgage:

Lowest cost

First priority claim

Strong covenant constraints

Debt service:

DebtServicet=Interestt+AmortizationtDebtService_t = Interest_t + Amortization_tDebtServicet=Interestt+Amortizationt

4.2 Mezzanine Debt

Subordinate financing:

Higher interest

Often interest-only

Secured by equity pledge

Cash flow priority:

Senior→Mezz→EquitySenior \rightarrow Mezz \rightarrow EquitySenior→Mezz→Equity

4.3 Preferred Equity

Hybrid instrument:

Fixed preferred return

Paid before common equity

No foreclosure rights but control provisions

Preferred return:

PrefReturnt=rp⋅PrefCapitalPrefReturn_t = r_p \cdot PrefCapitalPrefReturnt=rp⋅PrefCapital

4.4 Common Equity + Promote

Sponsor equity earns upside through promote:

Example split:

LP receives 70%

GP receives 30% promote above hurdle IRR

Promote introduces convex payoff structures.

(See Section 7 for IRR nonlinearity.)

5. Waterfall Mechanics as Conditional Allocation Functions

5.1 Piecewise Distribution Rules

Cash flow allocation is piecewise:

Distt={PayDebt,CFt<DebtServicetPayPref,CFt>DebtServicetPayPromote,IRR>HurdleDist_t = \begin{cases} PayDebt, & CF_t < DebtService_t \\ PayPref, & CF_t > DebtService_t \\ PayPromote, & IRR > Hurdle \end{cases}Distt=⎩⎨⎧PayDebt,PayPref,PayPromote,CFt<DebtServicetCFt>DebtServicetIRR>Hurdle

This creates discontinuities in return profiles.

5.2 Example Waterfall Sequence

Assume:

NOI = $10M

Debt service = $6M

Remaining = $4M

Steps:

Pay preferred return: $2M

Return equity capital: $1M

Excess $1M split 70/30

GP promote = $0.3M

LP distribution = $0.7M

6. Waterfall Optimization Problem Formulation

6.1 Objective Function

Sponsor wants to maximize equity IRR:

maxIRRequity\max IRR_{equity}maxIRRequity

Subject to:

DSCR constraints

Preferred return obligations

Reserve requirements

Refinance limits

6.2 Optimization Constraints

Core constraint:

DSCRt≥1.25DSCR_t \geq 1.25DSCRt≥1.25

Liquidity constraint:

CashReservet≥ReserveminCashReserve_t \geq Reserve_{min}CashReservet≥Reservemin

Preferred equity constraint:

DCFt≥PrefReturntDCF_t \geq PrefReturn_tDCFt≥PrefReturnt

6.3 Decision Variables

Optimization levers:

Debt sizing

Interest-only vs amortizing

Refinance timing

Capex scheduling

Promote hurdle design

7. Nonlinear IRR Dynamics in Promote Structures

7.1 IRR Definition

Equity IRR solves:

0=∑t=0TCFt(1+IRR)t0 = \sum_{t=0}^{T} \frac{CF_t}{(1+IRR)^t}0=t=0∑T(1+IRR)tCFt

Promotes make cash flow asymmetric:

downside capped at loss

upside convex for GP

7.2 Promote Hurdle Example

If hurdle = 12% IRR:

Below 12%: LP gets 90%

Above 12%: GP promote increases to 30%

Thus:

DistGP={0.10CF,IRR<12%0.30CF,IRR>12%Dist_{GP} = \begin{cases} 0.10CF, & IRR < 12\% \\ 0.30CF, & IRR > 12\% \end{cases}DistGP={0.10CF,0.30CF,IRR<12%IRR>12%

This is equivalent to an embedded call option.

(See Topic 5 real options valuation.)

8. Dynamic DSCR Forecasting Under NOI Volatility

DSCR is stochastic because NOI is stochastic.

DSCRt=NOItDebtServicetDSCR_t = \frac{NOI_t}{DebtService_t}DSCRt=DebtServicetNOIt

NOI variance drives DSCR breach probability:

P(DSCRt<1.0)P(DSCR_t < 1.0)P(DSCRt<1.0)

Thus, optimization must incorporate NOI-at-risk.

(See Topic 2 Section 9 and Topic 9 deep dive.)

8.1 Monte Carlo DSCR Simulation

Simulate NOI paths:

NOIt(j)NOI_t^{(j)}NOIt(j)

Compute DSCR paths:

DSCRt(j)=NOIt(j)DebtServicetDSCR_t^{(j)} = \frac{NOI_t^{(j)}}{DebtService_t}DSCRt(j)=DebtServicetNOIt(j)

Then estimate:

Expected DSCR

Tail breach probability

Covenant stress scenarios

Example Output

Metric | Value |

|---|---|

Mean DSCR | 1.38x |

5th percentile DSCR | 1.05x |

Breach probability (<1.20x) | 18% |

9. Waterfall Stress Testing and Tranche Risk

9.1 Tranche Loss Allocation

In downturns, losses absorb bottom-up:

Common equity wiped

Preferred impaired

Mezz defaults

Senior threatened last

Expected loss per tranche:

ELi=PDi⋅LGDiEL_i = PD_i \cdot LGD_iELi=PDi⋅LGDi

Where:

PD = probability of default

LGD = loss given default

9.2 Cash Sweep Triggers

Many loans impose cash sweeps if DSCR falls:

DSCRt<1.15⇒Sweep=100%DSCR_t < 1.15 \Rightarrow Sweep = 100\%DSCRt<1.15⇒Sweep=100%

This removes equity distributions and accelerates deleveraging.

10. Asset Optimization Through Waterfall Engineering

Waterfall modeling enables optimization beyond financing.

10.1 Capex Timing

Capex reduces NOI temporarily but increases long-term rent.

Optimize:

maxIRR subject to DSCR stability\max IRR \text{ subject to DSCR stability}maxIRR subject to DSCR stability

10.2 Refinancing Strategy

Refi resets debt service:

DebtServicenew<DebtServiceoldDebtService_{new} < DebtService_{old}DebtServicenew<DebtServiceold

Improves DSCR and unlocks equity distributions.

10.3 Preferred Equity Restructuring

Refinance out expensive pref:

reduces fixed obligations

increases free cash flow

stabilizes waterfall

11. Portfolio-Level Structured Finance Optimization

At portfolio scale, managers optimize across assets:

max∑wiIRRi\max \sum w_i IRR_imax∑wiIRRi

Subject to:

portfolio DSCR minimum

liquidity coverage

correlated vacancy shocks

Diversification reduces tranche-level tail risk.

(See Topic 10 portfolio optimization.)

12. Summary of Key Technical Takeaways

Component | Model | Output |

|---|---|---|

Waterfall allocation | Priority sequencing | Distribution rules |

Key KPI | DSCR | Covenant compliance |

Promote convexity | Piecewise IRR | Sponsor upside |

Optimization | Constrained maximization | Capital efficiency |

Stress testing | Monte Carlo DSCR | Breach probability |

Tranche risk | Loss allocation | Structured downside |